Back in 2020, Dubai International Financial Centre (DIFC) introduced the DIFC Employee Workplace Saving scheme, better known as DEWS. DEWS essentially restructured the old ‘defined benefit’ (DB) End-of-Service gratuity plan in the DIFC into a funded ‘defined contribution’ (DC) plan.

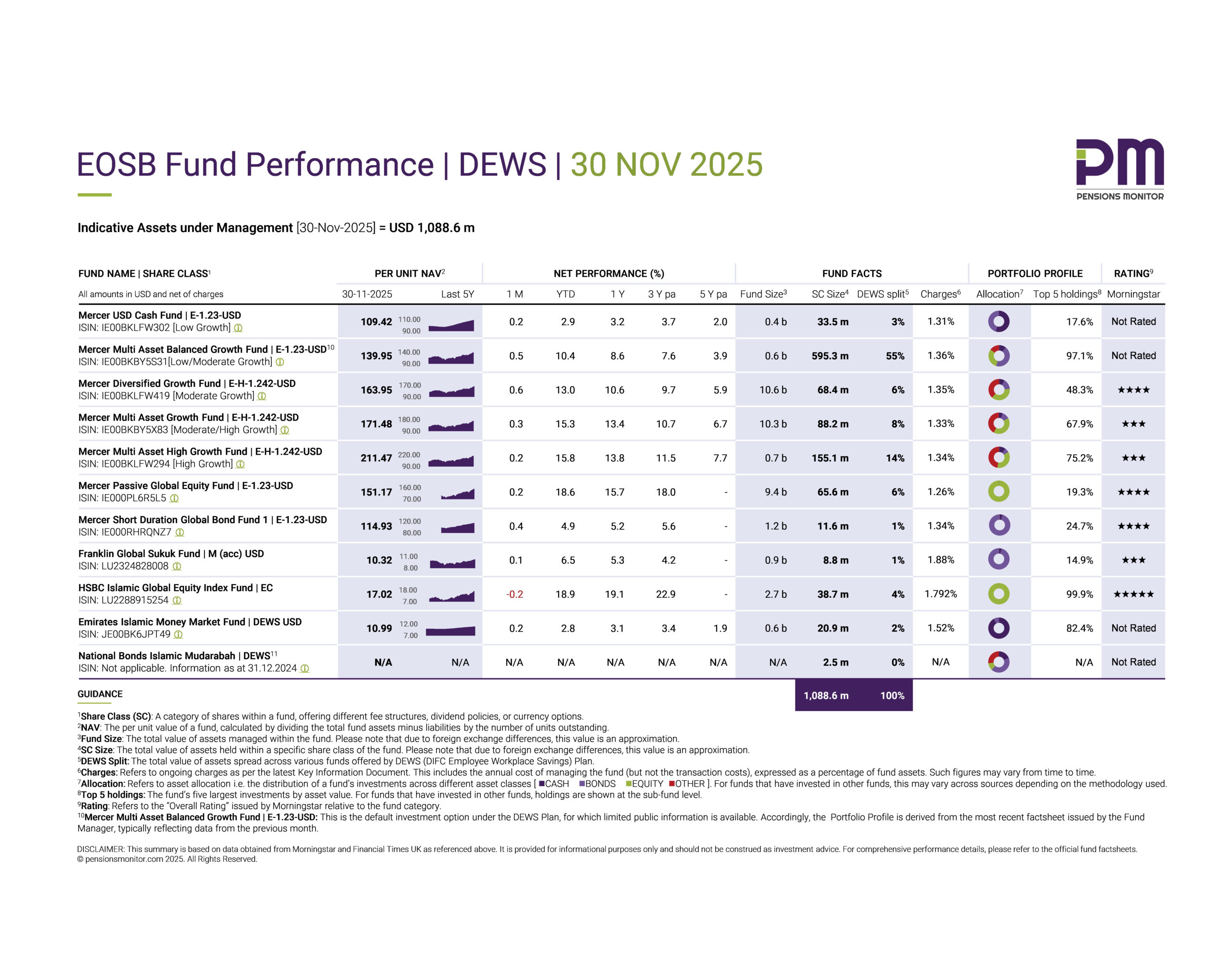

In short, employers pay a percentage of employee wages as monthly contributions and each employee decides into which funds these contributions will flow. The scheme currently has 10 funds to choose from with varying risk-return profiles as below.

The scheme also offers a voluntary savings plan allowing employees working in the DIFC to top up their savings with ease and was further extended to expatriate employees of Dubai Government entities in 2023.

In terms of performance, DEWS has accumulated a significant amount of funds in a short period of four years growing from USD 119mn with 18,057 employees at YE 2020 to USD 555mn with 41,590 employees (including 10,122 Dubai government employees) at YE 2023.

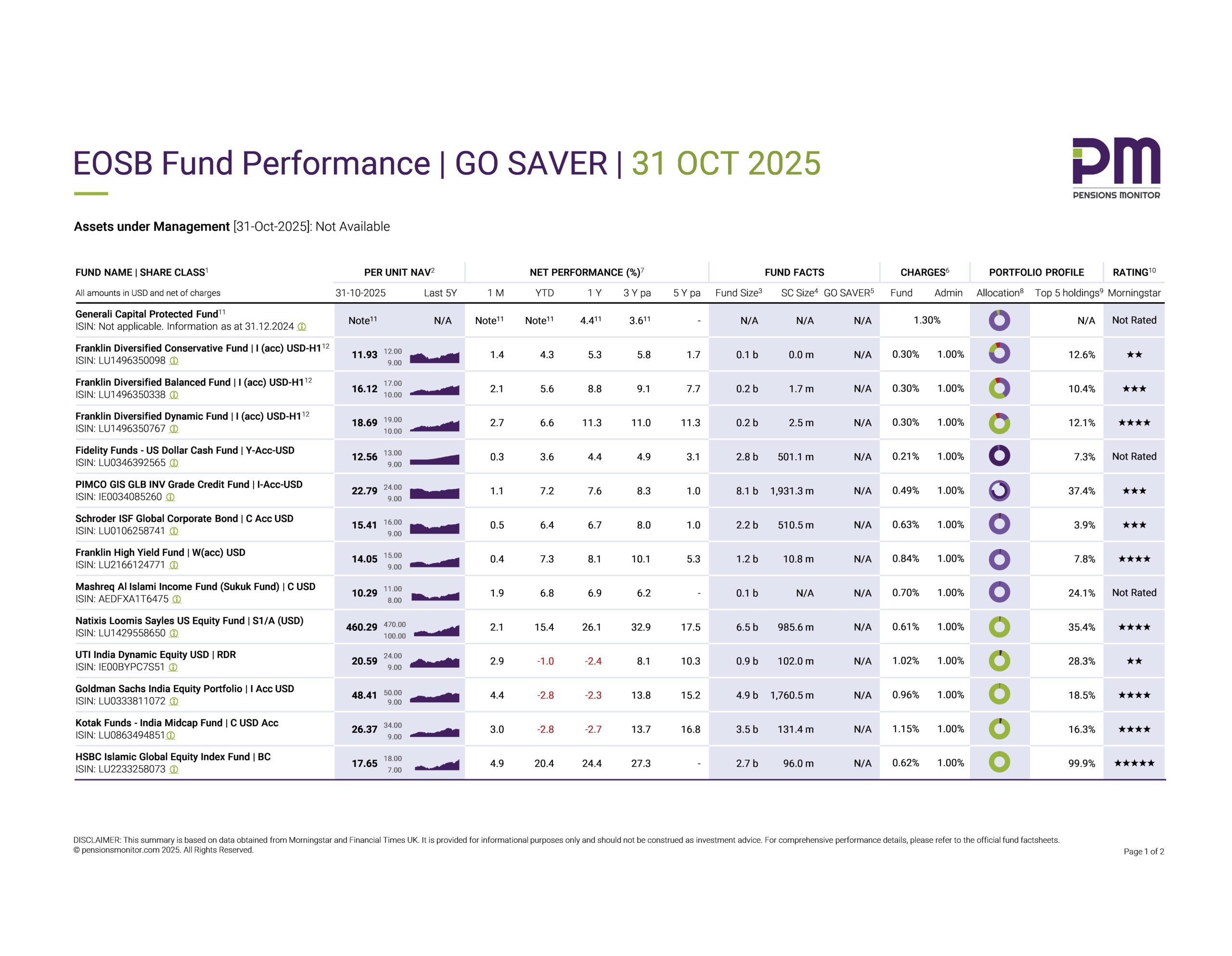

MOHRE’s End-of-Service Saving Scheme (EoSS) is similar to DEWS in that both schemes are funded and both schemes allow employees to choose between different investment options. However, there are a number of key differences:

Choice of provider

At present there is only one provider in the DIFC (Zurich) whereas MOHRE’s mainland scheme is expected to have multiple providers giving employers more choice. It should be noted that SUKOON has obtained a license to offer a DEWS scheme in the DIFC in 2023, however, operations are supposedly yet to start.

Scheme structure

DEWS is delivered through three companies, each with different roles and responsibilities with Equiom as the Trustee effectively having the oversight over the scheme, Zurich Workplace Solutions Middle East, part of the global insurance giant Zurich, as the Plan Administrator and Mercer as Investment Adviser to choose and monitor the investment funds. This is akin to leading global practices.

For MoHRE’s mainland scheme, however, there is no control by an independent investment adviser, or Trustee. The closest equivalent on the mainland is the custodian who is obliged to ensure that the decisions made by the fund manager are in the best interests of the beneficiaries. How this will work in practice remains to be seen, as this goes beyond the classical role custodians generally perform.

This difference raises many questions: Who ensures that the funds on offer are suitable? And offer good value for money? And are well-performing?

Fund choices

The DEWS scheme offers multiple funds from multiple fund managers. This enables the Investment Adviser to pick “best of breed” funds. For e.g. a Shariah sukuk fund from Fund Manager A, a global growth equity fund from Fund Manager B, and so on. On the other hand, the mainland scheme according to MoHRE sees a single Fund Manager in charge offering its own funds. This, in our opinion, severely limits choice and possibly leads to underperforming funds being offered to employees. For instance, Fund Manager C might have an excellent Shariah sukkuk fund, however, its global growth equity fund might perform below benchmarks. Under the new Mainland rules, Fund Manager C will offer both funds to employees, and those choosing the equity fund will therefore achieve growth below benchmark.

An alternative could involve SCA allowing the plan administrator to offer multiple (SCA-approved) funds from multiple providers, thereby replicating the fund choice that DEWS offers. This is yet to be seen in the market place, and such an idea would first need to be tested with the relevant regulators.

Cost

The fees associated with DEWS are relatively high at 1.35% on Assets under Management compared to the pension charge cap of 0.75% in the UK for instance. This is partly because there are three participants involved in DEWS – plan administrator, investment adviser, and Trustee (plus of course, fund managers and their administrators).

Fees for MoHRE’s mainland scheme on the other hand have been capped at 1.0% for the “default” capital guarantee option while the risk-based funds will likely carry higher fees.

Legacy End-of-Service benefit

Another aspect of contrast is the accrued unfunded end-of-service benefit up and until the date of switchover to the new scheme. With DEWS, the accumulated days are multiplied with the latest salary while for the mainland, the accumulated days will be multiplied with the salary at the time of switch-over. This means DEWS is more generous, taking into account salary increases that happen after the switching over to the new scheme.

In conclusion, DEWS is a professionally managed plan that has been structured in line with leading global practices although the charges are fairly steep whereas MoHRE’s mainland rules provide for a broad latitude of options for employees although this could unfavourably impact fund choices, fund quality and fund performance.

Finally, Cabinet Resolution 96 states that the conditions and obligations set forth therein apply to approved free zones that will be implemented in coordination with the relevant authorities within the financial free zones to determine which standards and obligations will be supervised and implemented by the freezone authorities on behalf of MOHRE or SCA. In other words, it is likely that DEWS itself may alter in due course in order to be compliant with Cabinet Resolution 96.

Follow Pensions Monitor for more share insights on UAE’s developing pension industry.