Last year, we wrote about End-of-Service Benefits (EOSB) Contributions paid to funds being an allowable expense for Corporate Tax (CT) purposes, subject to certain conditions.

To recap: On the basis of Article 28 of the Federal Decree-Law No. 47 of 2022 (CT Law) that sets out the general rules for allowing deductions from profits for CT, EOSB contributions would normally be an allowable deduction for CT purposes, provided they are incurred wholly and exclusively for the purposes of the business, within the specified limit, and paid in the relevant tax period.

That said, we also noted that more regulatory clarity was needed as to which funds qualify. The CT Law currently does not specify clear criteria for qualifying funds, neither does it state whether the fund to which employer contributions are paid, should be domiciled in the UAE and subject to local regulations. Click here to read the full article.

Now that the first corporate tax cycle (for financial years starting 1 June 2023) is underway, with returns due from 28 February 2025 onwards, we are exploring whether companies have acted on this in practice. And if so, what is the procedure to claim such deductions? To find out, we spoke to a few companies, auditors and EOSB industry participants.

Here’s what we found on the ground.

UAE EOSB Savings Scheme

Providers (fund managers) of the official EOSB savings scheme regulated jointly by the Ministry of Human Resources and Emiratisation (MOHRE) and the Securities and Commodities Authority (SCA) were first licensed in July 2024. Even so, it took some months for these providers to go live, meaning that the UAE EOSB Savings scheme was not yet operational during the first tax year (June 2023–May 2024) for which the first returns have just been submitted.

In fact, records indicate that the first employer was registered in the scheme in October 2024. If this is the case, then the true test of deductibility for EOSB contributions will likely come with the September 2025 filings, at the earliest.

What about the DIFC?

The Dubai International Financial Center (DIFC) replaced EOSB gratuity with a mandatory EOSB Savings Scheme back in 2020, well before the (optional) UAE EOSB Savings Scheme was introduced.

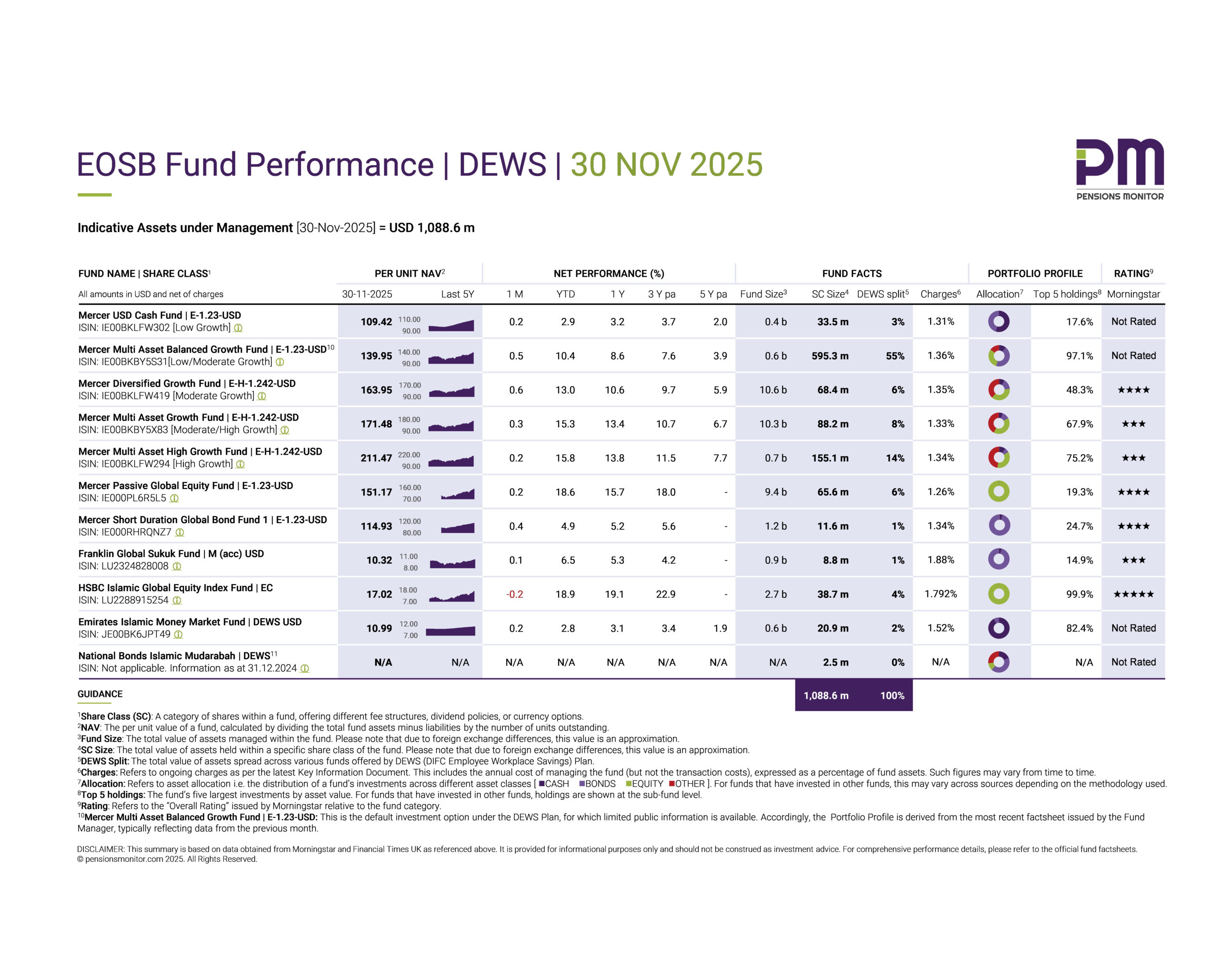

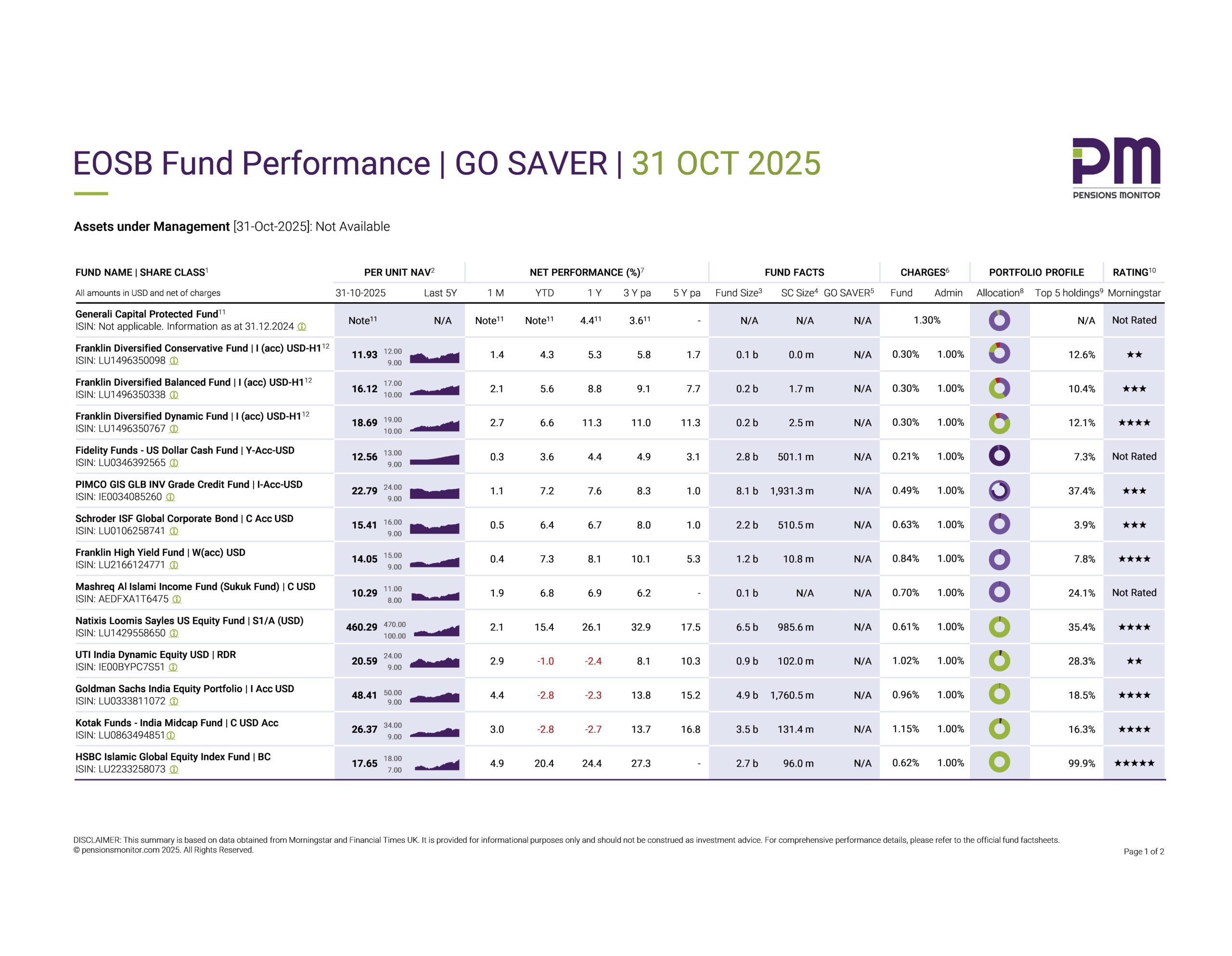

Some DIFC companies are also subject to the UAE CT Law, with filings due in 2025 for financial years beginning in 2023. Based on our conversations, companies understand that EOSB contributions to qualifying plans in the DIFC (e.g., DEWS or GO SAVER) are a legal requirement incurred wholly and exclusively for the purposes of the business and are therefore, deductible. As for the procedure, the understanding is that the digital nature of DEWS and GO SAVER platforms ensures a solid audit trail of calculations, payments, and statements that should suffice for CT purposes.

This aligns with practices in more established tax and pension jurisdictions, where evidence required for employer pension deductions typically includes payment records showing contributions to a registered/qualified pension scheme, payroll documentation indicating the employer’s pension contribution, and provider statements. In fully digital systems, real-time submissions reduce the need for additional paperwork. In others, like the U.S. or India, supplementary forms may be required.

Voluntary schemes

But apart from the official schemes, there are also other voluntary EOSB Savings products in the UAE that have been operational for years. Have companies contributing to these schemes claimed CT deduction?

We were not able to obtain clarity on this, however, we suspect that, if at all EOSB contributions to unofficial schemes qualify for CT deductions, a key condition would be the legal irrevocability of the employer’s contributions.

What about pension contributions for Emirati nationals?

Here the rules are clear and directly referenced in Ministerial Decision 115 of 2023.

Pension contributions for Emirati nationals have long been mandatory under Federal Law No. 7 of 1999. Employers must contribute to government-managed schemes like the General Pension and Social Security Authority (GPSSA) and Abu Dhabi Pension Fund (ADPF). Since these payments are legally required and processed digitally, companies have been advised by tax advisors that these records are sufficient for CT deductions.

So where does this leave us?

At present, there is no formal guidance from the Federal Tax Authority (FTA) specifying which EOSB savings schemes/funds qualify for CT deductions, or how such deductions should be claimed.

From our limited research, we have not identified any employers who have successfully claimed EOSB contributions as a deductible expense and received confirmation from the FTA, that could serve as a public precedent.

But if you, dear reader, have insight into this, perhaps your company has filed or received informal guidance from auditors or the FTA, then please write in to us at info@pensionsmonitor.com. Your experience could help others navigate this uncharted space.

In the meantime, here are a few practical tips for companies gearing towards EOSB Savings Schemes:

- Ensure the EOSB savings scheme represents a genuine, irreversible outflow of economic resources for the employer i.e., properly documented, legally irrevocable, held with a licensed and regulated provider, and clearly earmarked as an employee benefit.

- Keep your payroll, compliance, and accounting records aligned with Article 56 of the CT Law and Cabinet Decision No.74 of 2023 and ensure they are audit-ready.

- Consider engaging tax advisors or requesting a private ruling to clarify your specific circumstances.

As more companies transition to savings schemes, we hope that the FTA will issue public clarifications to support consistent tax treatment across the board.

Sign up for our free newsletter

We hope you found this article useful. Do write to us if you have any questions on the topic and don’t forget to sign up for our free newsletter to stay on top of all things End of Service Benefits.