The Registration Authority (RA) of the international financial centre of Abu Dhabi – ADGM (Abu Dhabi Global Market) has published new employment regulations (the Employment Regulations 2024) which reflect global changes in workplace practices.

The new rules (available for download below) will come into effect on 1st April 2025, thereby granting employers sufficient time to align their internal policies, employment contracts and other employment-related practices.

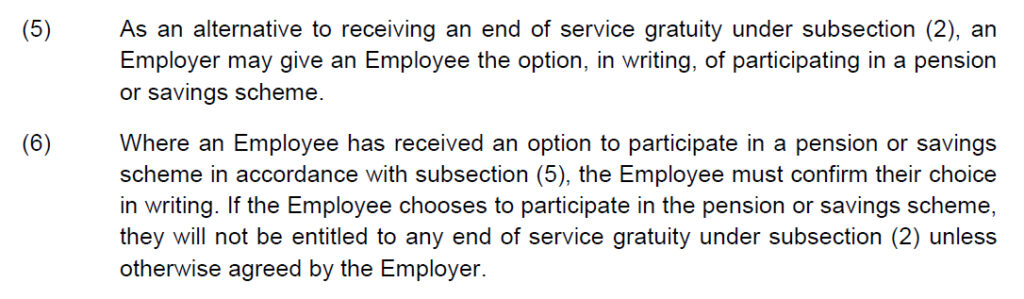

Of particular importance are Clauses 5 and 6 of Article 61 (“End-of-Service Gratuity”) that is reproduced below. In effect, it enables employers to replace the current End-of-Service Gratuity system with a pension or savings scheme.

As per the wording of the new Employment Regulations, the transfer to a pension or savings scheme is “double voluntary” – companies can give employees the option to participate; and employees may in turn sign up if they wish (or not).

However, it is unclear as to which schemes qualify in ADGM – the mainland scheme (approved by MOHRE and SCA) or whether the DIFC scheme qualifies as well, noting that both these schemes bear certain differences. We discussed these differences in a previous article in detail but below is a refresher in light of the current market developments:

- Scheme structure: The DIFC scheme is delivered by a Plan Administrator, Investment Advisor and a Trustee that effectively oversees the scheme, akin to leading global practices. Whereas for the mainland scheme, there is no control by an independent investment advisor, or a Trustee. The closest equivalent on the mainland is the Custodian, who is obliged to ensure that the decisions made by the fund manager are in the best interests of the beneficiaries. This typically goes beyond the classical role custodians generally perform.

- Choice of providers: At present, there are four providers for the mainland scheme. All of them were approved in second half of 2024 and we understand that some of the providers are not yet fully operational. On the other hand, DIFC has two fully operational plans – DEWS which has been servicing companies since 2020 and the brand-new GO SAVER plan by Sukoon Workplace Savings that is also fully operational now.

- Flexible multi-provider option: DIFC permits employers to sign up with more than one provider and allocate employees across the two plans if desired, whereas the mainland scheme restricts companies to a single provider, forcing a uniform provider choice across the organization.

- Fund choices: DIFC plans offer multiple funds from multiple fund managers. This enables the Investment Adviser to pick “best of breed” funds. In contrast, the mainland scheme features a single Fund Manager in charge, and offering its own funds. This, in our opinion, severely limits the fund choices for the mainland scheme and could possibly lead to underperforming funds being offered to employees. Moreover, at present, the mainland providers have only capital protected funds on offer.

- Charges: The fees associated with DIFC plans are relatively higher and in excess of 1.00%. This is partly because of the operating structure of the scheme involving a plan administrator, investment adviser, and Trustee (plus of course, the respective fund managers and their administrators). In comparison, we understand that fees for the mainland scheme have been capped at 1.0% for the “default” capital guarantee option while the risk-based funds will likely carry higher fees.

- Treatment of accumulated EOSB on transition: The DIFC regulation is also more generous with respect to the accumulated EOSB. Here the accumulated days as at the date of transition is multiplied with the latest basic salary, whereas for the mainland, the accumulated days is multiplied with the basic salary at the time of switch-over.

Regardless of the scheme that ADGM decides to adopt, the new Employment Regulations is an excellent and positive development for all employees in ADGM, as in the long run, savings schemes are generally superior to the existing gratuity mechanism.

Pensions Monitor is closely tracking EOSB developments at ADGM and we will share updates with our readership as soon as we hear more. Do sign up for our free newsletter.